FX Risk Management as a Value Driver

Matthias Hund has been with BELLIN since 2012. As a Consulting Director, he’s mainly responsible for system implementation and process consulting projects.

Matthias Hund joined BELLIN from PWC’s Financial Services unit. He studied Business Administration in Ingolstadt and Mannheim and specialized in Finance and Accounting.

Businesses have various means of boosting their profitability. Traditionally, they achieve this by increasing their turnover or by reducing costs. Another option is the introduction of efficienttreasury management, but while the first two possibilities are common knowledge and generally accepted, corporate management has yet to fully embrace the value of treasury. This is despite the fact that treasury management harbors potential that businesses are able to leverage without outside help. Efficient treasury management gives them a means of proactively influencing their profitability.

This post briefly outlines how treasury departments are set up before looking at the value of currency risk management.

Responsibilities and structures of treasury management

The ultimate responsibility of treasury management is to guarantee long-term business survival and to ensure a company is always able to meet its financial obligations. This makes treasury a crucial success factor for any business. But can we actually quantify the value it contributes? Financial departments are under enormous pressure when it comes to costs. In turn, it should be in treasurers’ own interest to be able to highlight the significant sums that their work can contribute both through cost savings and by mitigating earnings volatility.

Generally, we can distinguish between profit-oriented and service-oriented treasury activities – and both can enhance the value of a business. Profit-oriented activities include FX trading or speculative deals. They have a direct impact and generate additional earnings through active treasury management. Service-oriented activities on the other hand, for example, group-wide liquidity management, have an indirect impact by adding value to the different business segments. In most companies, treasury departments are set up as service centers, and it is these companies I would like to focus on in my evaluation of the value they contribute. This value is not always immediately apparent.

Take for example intercompany netting: one of the benefits of introducing netting is that it enables businesses to lower the volume of payments and to save on transaction costs for all group companies involved in the netting process. Based on identified value contributions, it is possible to deduce defined key figures to measure value, such as the percentage of entities involved in the netting process or Key Performance Indicators (KPIs). For a company, KPIs are the best means of managing treasury performance as they operationalize business objectives and reflect the underlying treasury strategy.

How to quantify value contributions

So how can we quantify the value treasury contributes? Let’s take a fictitious yet realistic example with concrete figures: the company “Supplier plc.” Supplier plc. is a globally active group with FX flows and international payments. Their financial profile can be summed up as follows:

- Turnover: EUR 1.5 billion

- EBIT: EUR 70 million

- EBT: EUR 50 million

- Borrowed capital: EUR 500 million

Of which long-term borrowed capital: EUR 200 million

Of which short-term borrowed capital: EUR 80 million - Equity: EUR 300 million

- Liquid assets: EUR 30 million

- 20 offices in 10 different countries

- 5 different currency areas: Euro (EUR 50%), US Dollar (USD 20%), Pound sterling (GBP 10%), Japanese Yen (JPY 10%), Swiss Franc (CHF 10%)

- Average borrowing rate: 4.0 %

- Average investment rate: 0.5 %

- Average gross payment volume (incoming and outgoing) per year: EUR 1.5 billion

- Gross intercompany payment volume per year: EUR 0.75 billion

- Number of intercompany payments per year: 120,000

- Number of group-wide bank accounts: 80 (an average of 8 per group entity)

- Cash pools: 1 EUR zero-balancing cash pool, pooling the EUR entities

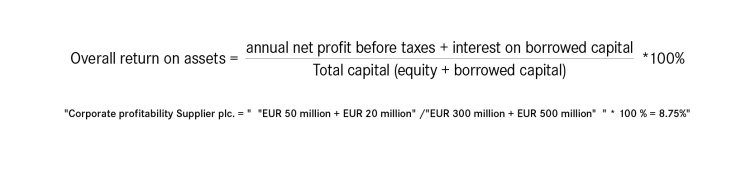

Value contributions refer to the overall corporate profitability and are evaluated under that aspect. This means we first need to work out the corporate profitability based on Supplier plc.’s figures:

How currency risk management increases corporate profitability

For treasury departments who use currency risk management instruments, we are able to calculate the exact value they contribute to corporate profitability, for example when currency forwards or options are used.

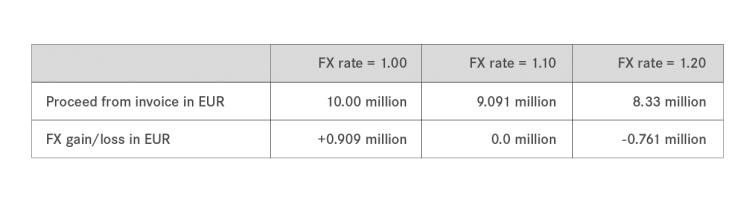

Let’s say Supplier plc. has sold equipment worth CHF 10 million to a Swiss company but production costs are incurred in euros. The payment is due exactly one year from the invoice date. For Supplier plc. this represents an FX receivable worth CHF 10 million, and they would like to mitigate the associated risk by means of a currency forward contract. Supplier plc. makes a forward sale of CHF 10 million and a purchase to the respective countervalue in euros at the prevailing forward rate. The forward rate is fixed at EUR/CHF 1.10. Upon expiration of the FX Forward contract, the following payments are made:

- Incoming amount from Swiss company based on invoice: + CHF 10 million

- Uutgoing amount in CHF based on Forward contract: – 10 CHF million

- Incoming amount in EUR based on Forward contract: + EUR 9.091 million (1/1.1=0.9091)

Irrespective of any hedging, this amounts to net proceeds of roughly EUR 9.091 million. The following table illustrates how changed forward rates influence the deal for Supplier plc.

Should the final forward rate amount to exactly EUR/CHF 1.10, then the deal results in no FX gains or losses for Supplier plc. However, it is definitely realistic to assume a volatility of around 10% for the currency pair EUR/CHF over the course of one year. For the purpose of our example, let’s assume that the Swiss Franc rate recovers to EUR/CHF 1.20. In this scenario, entering into a currency forward contract prevented Supplier plc. from incurring an FX loss of EUR -0.761 million.

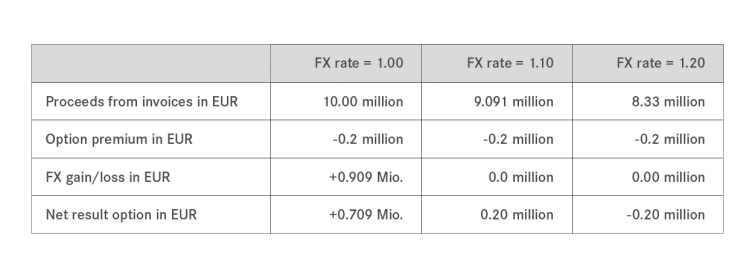

At the same time, eliminating all FX losses goes hand in hand with not realizing any FX gains, in our example EUR 0.909 million. In this context, currency options are an exchange rate risk hedging instrument that can prevent this. Again taking the example of a receivable of CHF 10 million, a currency option would result in the following: the strike price is fixed at EUR/CHF 1.10 (just like the forward rate), the currency option has a lifetime of one year, and a realistic value of EUR 0.02 per Franc (2%) is assumed as option premium. This option grants the right to sell CHF 10 million at a rate of EUR/CHF 1.10.

If the rate appreciates in favor of Supplier plc. (EUR/CHF 1.00), then they evidently benefit, underlining the advantages of a currency option. Options are unconditional forward contracts: you obtain the right but not the obligation to exercise them. This means that despite a premium of EUR 0.2 million, an option gives a company the chance to realize additional gains of 0.709 million. The option premium buys them the right to let the option expire without exercising it in case of adverse rate movements not favorable to the company (EUR/CHF 1.20). Options are therefore a means of mitigating losses but still potentially realizing gains. The main difference between a currency option and a currency forward is the speculative nature of the contract. You obtain the right to exercise the option but have no obligation to do so. Using realistic scenarios for the calculation of value contributions shows that both instruments have a positive influence on corporate profitability.

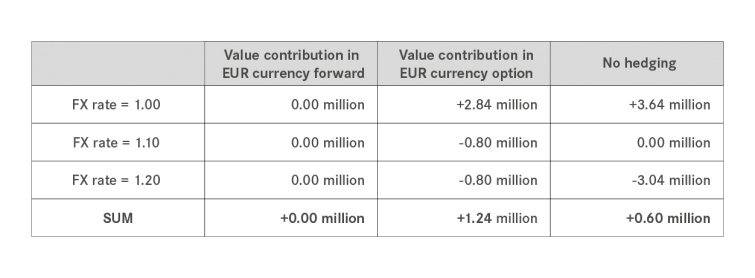

The calculations are based on the assumption that the described underlying transaction realistically occurs about once a month (invoice proceeds amounting to CHF 10 million). So over a time span of one year, this transaction occurs 12 times. In order to work out the value contribution of a forward contract compared to that of an option, we assume that potential FX rates occur with the same degree of frequency over the course of one year. Consequently, we are looking at four instances each of a EUR/CHF rate of 1.00, 1.10 and 1.20. Below table illustrates the gains and losses for Supplier plc. when making use of currency forward contracts or currency options.

The results indicate that currency forwards are mainly used to eliminate losses. They do not influence value contribution in the form of FX gains or losses, as losses are not possible and gains cannot be realized. The speculative currency option, on the other hand, results in an overall gain of EUR 1.24 million (given the same scenario) as it presents the option of capitalizing on appreciated rates.

If the rate matches the predicted scenario or falls short of it, then you can simply let the option expire. With the given rate development probability, not engaging in any hedging activities can produce a theoretical gain of EUR 0.6 million. However, you bear the full risk in case of a negative rate movement.

Conclusion: How the management of FX risks boosts a company’s profitability

We can conclude that in the unrealistic scenario of uniform distribution of exchange rates, the value contribution to corporate profitability is significantly higher for currency options than it is for currency forwards. This is due to the option presenting the chance to capitalize on opportunities whereas forwards merely mitigate risk.

For simplification purposes, we base our evaluation of currency risk management instruments (in terms of their contribution to corporate profitability) on the average value resulting from the figures for forwards and options. This is calculated as follows: (EUR 0.00 million + EUR 1.24 million)/2 = EUR 0.62 million. These EUR 0.62 million are added to the annual net profit. This results in the following corporate profitability development:

“corporate profitability = ” “EUR 50.62 million + EUR 20.0 million ” /”EUR 300 million + EUR 500 million” ” * 100 % = 8.83%”

The calculation shows that options and forwards can increase corporate profitability by 0.08 %. As we can safely assume that higher volumes entail better conditions and additional economies of scale, it is mainly larger businesses that are set to benefit financially from hedging activities.

Want to learn more about our powerful treasury solutions? Time to discover Coupa Treasury.