Putting a Figure on it – Examining the Profitability of Cash Pooling

Matthias Hund has been with BELLIN since 2012. As a Consulting Director, he’s mainly responsible for system implementation and process consulting projects.

Matthias Hund joined BELLIN from PWC’s Financial Services unit. He studied Business Administration in Ingolstadt and Mannheim and specialized in Finance and Accounting.

It is safe to say that treasury pays. And as treasurers, we think we can prove and quantify this claim. In a previous post in the "putting a figure on it" series, we were able to demonstrate the monetary value of interest management. Today, we will take a look at cash pooling to establish whether it also has a positive influence on corporate profitability – even in times of no or negative interest.

In the past, many companies introduced cash pooling to optimize interest results or to place overnight investments. Currently however, financial markets are characterized by high liquidity and low interest rates, and spreads between overnight money borrowed and overnight money invested have dramatically reduced or been completely turned on their head. With this development, the focus has shifted to safeguarding liquidity and to balancing liquid assets between different group companies. Cash pooling creates visibility throughout the entire group when it comes to liquidity, and this in turn allows businesses to reduce financing costs group-wide and to maximize corporate profitability that way. To demonstrate the positive monetary impact of cash pooling, I will once again use the example of fictitious Supplier plc., introduced in my previous posts on the value of interest and FX management as well as netting.

Supplier plc. is a globally active group with FX flows and international payments. Their treasury profile can be summed up as follows:

- Turnover: EUR 1.5 billion

- EBIT: EUR 70 million

- EBT: EUR 50 million

- Borrowed capital: EUR 500 million

Of which long-term borrowed capital: EUR 200 million

Of which short-term borrowed capital: EUR 80 million - Equity: EUR 300 million

- Liquid assets: EUR 30 million

- 20 offices in 10 different countries

- 5 different currency areas: Euro (EUR 50%), US Dollar (USD 20%), Pound sterling (GBP 10%), Japanese Yen (JPY 10%), Swiss Franc (CHF 10%)

- Average borrowing rate: 4.0 %

- Average investment rate: 0.5 %

- Average gross payment volume (incoming and outgoing) per year: EUR 1.5 billion

- Gross intercompany payment volume per year: EUR 0.75 billion

- Number of intercompany payments per year: 120,000

- Number of group-wide bank accounts: 80 (an average of 8 per group entity)

- Cash pools: 1 EUR zero-balancing cash pool, pooling the EUR entities

Corporate profitability Supplier plc. =8.75%

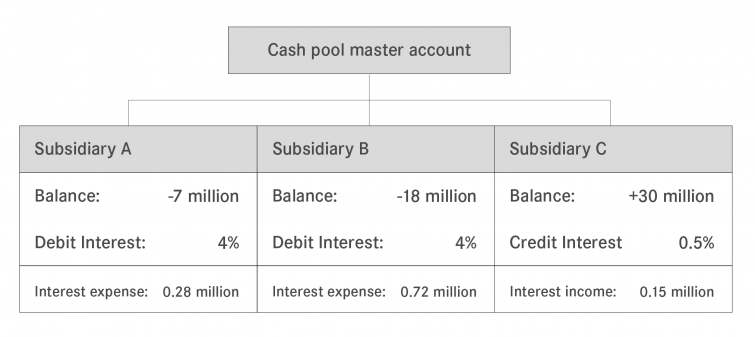

The elements that present the most leverage when it comes to boosting corporate profitability by means of cash pooling are debt financing (in particular short-term borrowed capital), average interest rates for short and long-term financing and investment interest rates. The following graph highlights Supplier plc.’s situation without effective cash pooling – quite a common scenario:

Subsidiaries A and B have a combined debit balance of EUR 25 million in debt financing, together generating a negative interest result of EUR 1 million. The positive credit balance of EUR 30 million on the other hand only generates EUR 0.15 million in interest income. Despite the overall balance across all three group companies being positive, the netted interest result is negative and amounts to EUR -0.85 million.

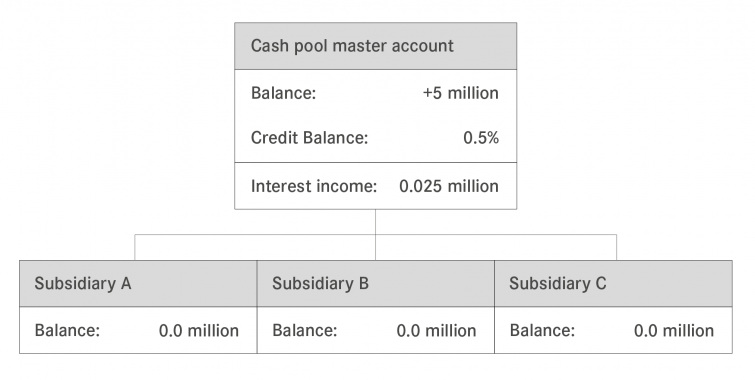

Given the same parameters, the use of a physical zero-balancing cash pool optimizes liquidity allocation:

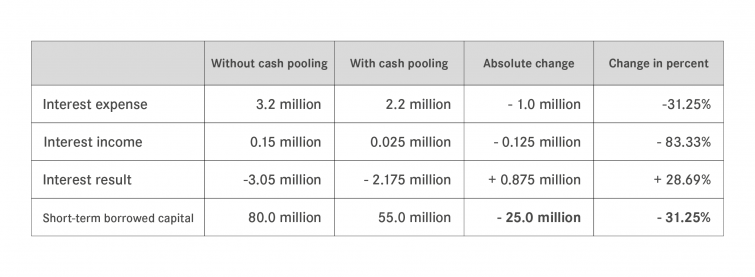

By physically transferring subsidiary balances to the parent company’s cash pool master account, the negative balance of subsidiaries A and B is offset, leaving a group-wide credit balance of EUR 5 million that generates EUR 0.025 million in interest income. Compared to our original scenario, the interest result can be improved by EUR 0.875 million. Next to improving their interest result, Supplier plc. is able to reduce short-term borrowed capital by EUR 25 million, as the liquid funds amounting to EUR 30 million are used to offset short-term borrowed capital. Expressing the change in percentage makes the case even more clear and convincing: by introducing cash pooling, the interest result could be improved by 28.69 percent, and group-wide short-term borrowed capital can be reduced by as much as 31.25%.

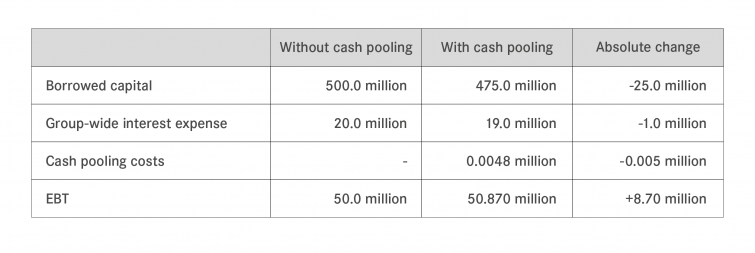

So how does the positive impact of cash pooling translate to corporate profitability? In order to establish this, we need to work out the impact of the interest result and the short-term borrowed capital following the introduction of cash pooling in relation to group-wide borrowed capital, group-wide interest expense and EBT.

The bank charges Supplier plc. for the administration of the cash pool, but these charges are negligible. Our experience with customers shows that a EUR zero-balancing cash pool costs around EUR 100 per month and per integrated account. Our example is based on a EUR cash pool with four accounts, resulting in a cost of EUR 4,800 per year. This figure has been included in below table and in the calculation of corporate profitability.

We had calculated Supplier plc.’s corporate profitability to amount to 8.75%. Including the figures listed in the table above following the introduction of a zero-balancing cash pool in the calculation, leads to the following result:

This shows that the introduction of a zero-balancing cash pool alone boosts group-wide corporate profitability by 0.27% per year.

Conclusion

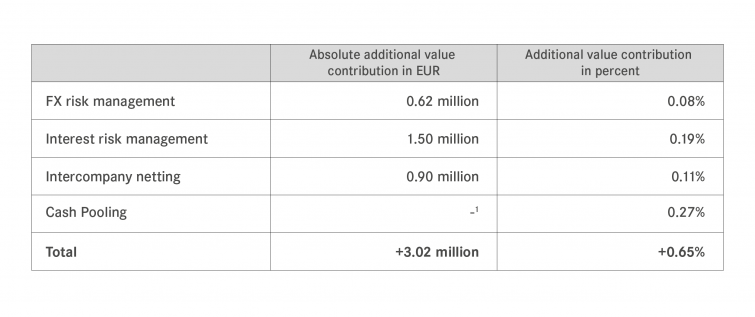

With this and the previous posts of this series, we have been able to demonstrate how the instruments of interest and FX management, netting and cash pooling can add value to a business and boost profitability. I was able to quantify this positive impact and worked out the following figures using the example of Supplier plc.:

This table clearly illustrates the value contribution to corporate profitability that an optimized treasury function can create. Contributions made through intercompany netting and cash pooling in particular are mainly based on process optimization, rationalization and cost optimization, i.e. these are figures that do not depend on speculative interest rate or FX rate developments. Given market fluctuations, contributions made through interest and FX risk management cannot be clearly quantified, but realistic scenarios and equal probabilities allow us to come to an approximate quantification.

All these figures show one thing: no business that is active on an international scale can do without a functioning treasury department that pays heed to current market developments! Ultimately, small and medium-sized enterprises are subject to the same risks as large groups. That said, they can also benefit from the mathematical consequences and positive results achieved through netting and cash pooling.

Treasury quality and performance have a substantial and direct impact on corporate profitability. Putting a figure on it and quantifying these amounts is a simple way of convincing management to provide additional resources for treasury. This will put treasury in a position where they can actually work strategically and achieve their full potential to the benefit of the whole business!

____________

1 It is not possible to work out an absolute value contribution in EUR for cash pooling, as cash pooling does not only translate to a reduction in expenses or an increase in revenue. Cash pooling also entails a reduction in borrowed capital which influences the denominator in the formula for the calculation of corporate profitability. Consequently, it is only possible to express improved corporate profitability in percent.

Want to learn more about our powerful treasury solutions? Time to discover Coupa Treasury.