Drive smarter spend strategies with AI

See what exceptional performance looks like and learn how to close the gaps.

Get the Benchmark Report

Drive smarter spend strategies with AI

The Total Spend Management Annual Benchmark Report

Trust is at the heart of the employee and company relationship. Most employees take this trust seriously, while others may exploit it. Take one Apple employee who stole over $17 million from the company. The employee used their position as a buyer for Apple’s supply chain to deploy a variety of employee fraud tactics, including receiving kickbacks from vendors, inflating invoices, and stealing repair parts.

If it can happen to an enterprise company like Apple, it can happen to any company. According to a global study, this kind of fraud impacts companies of all sizes at the same rate. Each year, it’s estimated that 5% of revenue is lost to it, with the average fraud case resulting in $1.6 million in losses. Companies big and small need the proper strategies to combat and prevent employee fraud.

Employee fraud, also known as occupational fraud, is the deliberate misuse of a company’s resources by an employee for personal gain. This type of fraud can take many forms, ranging from stealing inventory to inflating timesheets for a bigger paycheck. When fraudulent activity does occur, it results in financial losses (remember, on average, about $1 million), reputational damage among stakeholders, and operational disruptions from diverting critical resources.

There are a few common reasons an employee may turn to stealing, including:

Luckily for businesses, fraudsters also display certain behavioral characteristics that indicate signs of misconduct. In fact, 84% of fraudsters displayed at least one red behavior flag in fraud cases. The top five behavioral signs include: living beyond their means, financial difficulties, an unusually close relationship with a vendor, unwillingness to share duties, and irritability.

While all businesses face the challenge of employee fraud, some factors can make it easier to occur. Small and medium businesses often lack robust internal controls, leaving them vulnerable to manipulation. Certain industries, like financial services and public administration, tend to have the highest fraud cases due to access to large amounts of cash and sensitive data. And employee fraud may be more prevalent in industries with high inventory turnover (retail) or limited resources for monitoring (non-profits).

There are several common types of employee fraud to be aware of. Take this ploy, for example. A trio of conspirators worked together to try to steal $21 million from a major Australian bank through bank vouchers. Using her position of power, one employee issued blank vouchers to the two individuals in the hopes of manipulating the bank’s financial accounts for personal gain — a form of employee fraud known as asset misappropriation.

Common types of employee fraud include:

This is the most common form of employee fraud, where employees steal or misuse company assets. It includes stealing cash, inventory, equipment, intellectual property, or the unauthorized use of physical company property, such as a vehicle or tools. Asset misappropriation is very broad, so some other fraud types (billing schemes, expense reimbursement, etc.) fall under its umbrella.

Why it happens: Asset misappropriation covers many areas, so a lack of tracking and centralizing operational data increases a company’s risk. Poor inventory management for assets is another concern. Manual inventory management practices, such as physical cycle counting, make it harder to spot and stop theft from occurring. Asset misappropriation made up 89% of employee fraud cases in ACFE’s 2024 report.

When an employee manipulates the procurement process or colludes with external vendors for personal gain, it is a form of vendor fraud. The employee might:

Since vendor fraud can occur during the invoicing process, it’s sometimes considered invoice fraud.

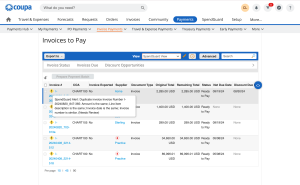

Why it happens: Manual or poor vendor management and accounts payable processes increase a company’s risk of vendor fraud. Cross-checking a vendor’s credentials against internal and external records and third-party risk is vital. Missing discrepancies between purchase orders and invoices is likely if you’re receiving thousands of invoices each month, working with various vendors, or battling a backlog of invoice approvals.

A Kia accounting department employee paid over $800,000 to a fake company she created and used the money to pay off personal credit cards. To avoid detection, she chose a company name similar to a real one that dealt with import duties on automobile shipments. This is a billing scheme — when an employee submits or authorizes fraudulent bills for payments. It’s also sometimes referred to as invoice fraud.

A few ways an employee might deploy this scheme are:

Why it happens: When one person is in charge of accounts payable, companies are more susceptible to billing schemes. It’s much easier for an individual to process fraudulent payments without proper oversight, such as multi-person approvals or department checks. In the ACFE’s 2024 occupation fraud report, billing schemes made up 22% of all asset misappropriation cases.

An employee buys an expensive bottle of cologne on a business trip and claims it’s a business expense for paper copies and presentation materials. They falsify his receipt and submit it. What they just committed is expense fraud, where employees claim false or inflated expenses for reimbursement. Employees might also try to get reimbursed for the same expense twice.

Why it happens: A weak verification process for submitting expense claims can make businesses vulnerable. The average expense fraud case lasts as long as 18 months before detection.

Payroll fraud occurs when an employee manipulates a payroll system to gain unauthorized compensation. An employee might create a “ghost employee” to pocket the wages. Or they might use the more common tactic of inflating their working hours, also known as timesheet fraud. They might add on a few hours here, tack on a few hours there, misclassify time to billed projects, or falsify approvals for time submissions.

Why it happens: Smaller companies might not have the proper controls or tools to cross-check payrolls, or larger companies might have such a large employee headcount that it can be difficult and time-consuming to check using manual measures.

Instead of disbursing $200,000 in scholarships to students, a college administrator diverts the money to his own personal account. This is an example of embezzlement, or account fraud, when an employee with access to funds or assets diverts them for personal gain. It might include unauthorized transfers from company accounts or misusing project funds.

Why it happens: It’s only natural to trust that employees are using authorized funds for the company. However, if there’s no cross-departmental check or segregation of duties for signing off on payments or cash disbursements, it’s possible to manipulate the system for personal gain.

Sometimes, employee fraud is not the act of stealing money. Financial fraud happens when employees or executives manipulate financial data to mislead stakeholders. They might overstate revenue to meet performance targets or underreport expenses to inflate profits.

Why it happens: The pressure to meet earnings expectations or receive performance bonuses are some of the main motivators behind this kind of fraud. Without a proper digital audit trail and segregation of duties, individuals may be able to manipulate records without detection.

Employee fraud can have a big impact on a business. The obvious ramifications are financial losses and reputational damage. However, one lesser-known consequence is the decline of strategic focus. It’s more difficult for defrauded companies to accurately forecast and plan, leading to poor budget and resource allocation. For example, fraudulent transactions may conceal expenses and cause leadership to make misguided investment and operational priority decisions. It can even lead to cash flow issues that make it impossible to fulfill customer orders, forcing customers to seek alternative brands.

Detecting and preventing employee fraud should be a top priority for every business. More than half of employee fraud cases occur due to a lack of internal controls, so focusing your efforts on this area is critical. Here are a few ways your company can enforce better internal controls to detect and stop fraud from occurring.

Segregation of duties (SoD) ensures that no one employee has complete control over multiple stages of a financial or accounts payable process. One employee may create the purchase order (PO), another approves it, and a third processes the payment. A multi-person approval approach is generally a good rule of thumb, especially when certain spend limits or thresholds are triggered.

Fraud becomes more challenging to execute because cooperation between multiple parties is required. Automated workflows add another layer of security. It enforces SoD by assigning responsibilities to different employees based on system roles and stops the next step in the process without a set of specific requirements. It’s much easier to manipulate paper-based processes. Digital workflows provide a clear audit trail.

💡Pro tips:

Integrating these source-to-pay processes ensures that all financial transactions are visible and linked within one system. For example, when an employee submits a vendor invoice, it can be cross-checked against a purchase order and previous payments automatically.

Fraud often occurs when processes are siloed, making it easy for employees to exploit gaps in the system. The integration provides a single source of truth across the entire transaction lifecycle, so when fraud detection software is deployed, it works much better with a holistic view of company funds. The software can also internally audit and check for discrepancies.

💡Pro tips:

When’s the best time to stop fraud? Before it happens. Manual methods of fraud detection, like periodic auditing, is a reactive approach. You’ll only spot fraud after the fact. AI-driven fraud detection helps you take a proactive approach and prevent it from happening before a payment is even made, stopping it in the first place.

AI uses real-time tracking to monitor transactions, flag anomalies, and identify patterns consistent with fraud. It’s much better at recognizing complex patterns that humans might miss. Let’s say an employee expensed over $1,400 for a recent work trip. That alone doesn’t raise any concern, but AI reveals something else — they’ve routinely expensed $700 more than the company average per trip. After the software flags this, you can look closer and verify their expenses.

Companies have the power to run continuous audits with AI to detect irregularities and fraudulent behavior as they happen rather than relying on periodic reviews. According to a recent study by PYMNTS Intelligence and Coupa, automated fraud detection systems outperform traditional, manual methods, yet just 28% of firms have adopted them.

💡Pro tips:

Virtual cards use a digital payment card generated for specific transactions or vendors. They have pre-built spending limits, expiration dates, and highly restricted usage rules. Instead of issuing corporate cards to employees, which offer limited fraud protection since they can be used freely, using a virtual card can reduce misuse since predefined parameters set spending. Additionally, virtual cards provide detailed transaction tracking, helping quickly identify suspicious activity.

💡Pro tips:

Despite recent advancements in fraud detection software, traditional methods like staff training programs remain popular. Automated software proves far more effective, however. Over 70% of respondents to PYMNTS and Coupa’s 2025 Certainty Project Report say automation is the most impactful strategy for reducing fraud. In contrast, just 27% say the same thing about staff training.

Modern fraud detection software relies on AI, machine learning, automation, and predictive analytics to analyze financial transactions and various operational data sources to detect fraud patterns as they occur. Integrating these tools within existing financial processes helps businesses proactively prevent fraud rather than just react to it after the damage is done.

Here’s how it works:

Software allows you to set up custom workflows that define how invoices, expenses, and payments are processed. Enforce approval hierarchies and role-based access that fit your company’s needs to ensure that no single employee has unchecked control over financial transactions.

Set up workflows for:

Coupa’s fraud detection software, SpendGuard™, uses dynamic approval flows that automatically add auditors for review when a transaction is flagged as noncompliant. It stops payments from being processed until proper approval is obtained. With drag-and-drop functionality, changes to workflows can also be made quickly and easily. Get the right people to review the right transaction at the right time to stop fraud before it happens.

Real-time compliance monitoring ensures spending adheres to company policies and external regulations by automatically checking transactions against preset rules. This includes off-contract spending, tax and duty policies, and even regulations like SOC 1.

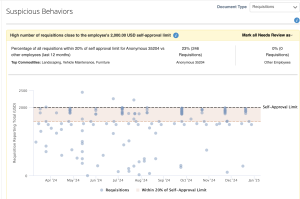

Let’s say you want to implement self-approval limits for requisitions to prevent employees from bypassing reviews. With SpendGuard, you can easily set up this rule and have it monitor processes across the procure-to-pay cycle. It doesn’t just protect against fraud. The increased visibility makes it possible to spot instances where an employee might actually need additional training and help (like if they’re constantly revising POs).

AI-driven fraud detection software constantly analyzes transactions, external vendors, and internal operational data to flag anomalies such as duplicate invoices, abnormal payment frequencies, or inconsistencies in employee expense reports. This monitoring happens in real time, so you can identify risks early.

SpendGuard enables you to see trends by:

SpendGuard uses $7 trillion in real-world transactions from the Coupa platform to provide predictive insights and spending patterns to stay one step ahead of fraudsters. The sheer volume and diversity of data across industries and company sizes enable Coupa’s AI to detect new techniques, provide contextual analysis for your specific industry, and differentiate between normal versus abnormal spending patterns to reduce false positives.

Decreasing the chances of false positives is also important to the employee-manager relationship. Imagine a new employee makes an honest mistake on an expense report that gets flagged by the manager as potential fraud. The manager then needs to confront the employee, and perhaps the employee has to reimburse the company, leaving a feeling of mistrust between both parties.

All of this can be avoided with AI-driven monitoring. When the expense report is created, the system flags it as “out of policy” and triggers the employee to adjust their expense report before submitting it. Software and automated logic are much better at enforcing fraud prevention because the rules are built in. This puts less stress on the manager to interpret fraud cases solely on their own, removing bias in the process and building trust between team members.

Traditional fraud detection uses periodic audits that happen monthly, quarterly, or annually to identify inconsistencies. It’s a human-led process that involves data collection, sampling, reconciliation and verification, and more. However, it has limitations in terms of accuracy and efficiency.

Fraud detection software replaces manual auditing efforts. Instead of periodic monitoring, it’s done in real time. It covers 100% of transactions, providing a larger sample size for more accurate results, and it’s cost-effective and scalable.

SpendGuard provides an auditing dashboard to inform users of risks across the procure-to-pay lifecycle. There are 25 alerts across six key categories (requisitions, purchase orders, invoices & payments, expenses, sourcing events, and timesheets).

For example, you might get an alert for a suspiciously low number of supplier bids on an event. Upon closer examination, one employee might be receiving kickbacks from this particular vendor since this employee has routinely selected this vendor for other high-value projects. Or an alert for misclassifying time from billing high-rate projects or falsifying approvals for time submissions might be flagged. SpendGuard analyzes timesheets to prevent reporting overtime for hours not worked.

Implementing fraud prevention software like SpendGuard ensures financial transactions are closely monitored, automated, and compliant with company policies. Proactively spot and stop employee fraud to protect your business and reputation among stakeholders and customers.

Oh! It looks like you opted out from using the needed cookies. If you are interested in using the AI Agent, then please opt-in to the cookies in the preference center.

Update preferences