Instant Payments, Faster Payments, Real-Time Payments and SWIFT gpi

In the age of digitization, we expect more from our services and technology: we want them to be available right then and there, in an instant, wherever we are – including payments services. So what is behind the names that promise just that: Instant Payments, Faster Payments, Real-Time Payments or SWIFT gpi? What opportunities do they present and what are their limitations? We take a closer look at these options as well as at a solution that holds great potential for businesses: EBICS SEPA Instant Credit Transfer and the SWIFT gpi technology with the SWIFT for Corporates project.

Instant Payments, Faster Payments, Real-Time Payments: What are they?

Definition Instant Payments and SEPA Instant Credit Transfer

Definition Faster Payments

Definition Real-Time Payments

Opportunities and limitations of real-time payment systems

What solutions do globally active businesses need?

SWIFT gpi: fast payments without borders

How SWIFT gpi works

The SWIFT for Corporates project

Payments in real-time: our conclusion

Instant Payments, Faster Payments, Real-Time Payments: What are they?

The need for faster payment solutions has been driving the development of new technology worldwide. While in many ways terms such as instant payments, faster payments and real-time payments are used interchangeably, three distinct official regional systems have been established: Instant Payments for the SEPA area, Faster Payments for the UK and Real-Time Payments in the US.

Definition: Instant Payments and SEPA Instant Credit Transfer

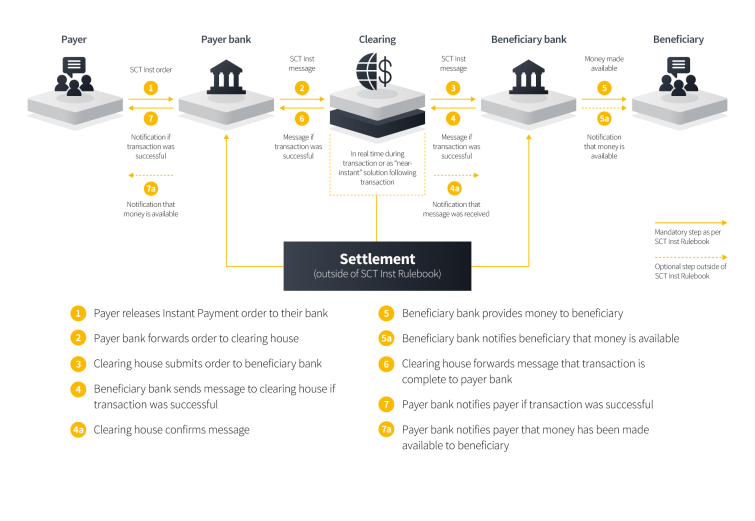

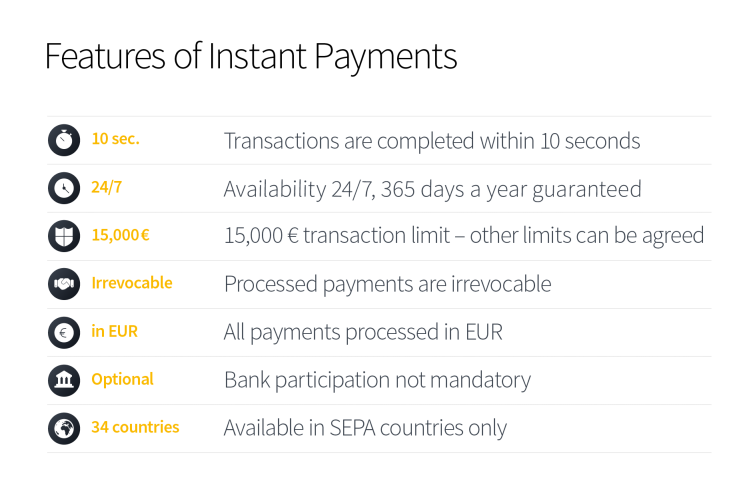

Instant Payments are electronic payments that are processed within seconds and credited from one bank to another without any intermediary. Both payer and payee receive immediate confirmation and the whole process is completed in under 10 seconds. Instant Payments can be processed at any time, 24/7/365. There is a 100,000 EUR transfer limit. Instant Payments are always single payments, and every transfer is irrevocable.

Using the European payments infrastructure, the Single Euro Payments Area (SEPA) has introduced the following Instant Payments system: SEPA Instant Credit Transfer (SCT Inst), developed by the European Payment Council (EPC). However, unlike for SEPA, participation in SCT Inst is not mandatory for financial institutions. This explains why some European banks have been offering Instant Payments for a while, while others have yet to communicate a date for when they will support the new system.

Starting November 2019, German banks that offer SEPA Instant Credit Transfer have to adhere to German Banking Industry Committee specifications for the EBICS channel. In the Coupa treasury management system, this is fully integrated and enables fast SEPA Instant Credit Transfer transactions. In the system, it is even possible to release them as bulk payments. In addition to direct processing of the payment order, the end-to-end status information available is particularly valuable for treasurers. After processing the real-time payment, the bank provides a report documenting the credit to the recipient. For Coupa’s corporate customers which use the EBICS channel, the new technology smooths the transition to the era of real-time payments and processing of end-to-end status messages for single and bulk payments.

Adapted from Deloitte

Adapted from Deloitte

Definition Faster Payments

The UK fast payments initiative dates as far back as the 1980s. The Faster Payments Service (FPS) is a quasi real-time system that was introduced by Pay.UK, the UK’s leading retail payments authority, in May 2008.

It is the UK’s 24/7 payments solution, with confirmations being issued within 15 seconds and the transaction completed within two hours maximum. FPS covers single payments, scheduled transfers, direct debits or bulk payments by companies with a direct connection to the service. Payment orders can only be processed in GBP. The limit for any one transaction is GBP 250,000 and can be lowered further by participating banks. Faster Payments transfers are also irrevocable.

Definition Real-Time Payments

In the US, the oldest banking association and payments company, The Clearing House (TCH), has been developing the real-time system “Real-Time Payment” (RTP®).

RTP is available 24/7 and works in the background, processing payments in real time. There is a 35,000 USD transaction limit. In addition to fast payment processing, RTP also enables participants to send messages. The system is set up in a way that technically allows all participants to make Real-Time Payments to each other: companies, consumers and public authorities. The system launched in 2017 and is open to all payment service providers. The aim is to provide access to the RTP network for all financial institutions by 2020.

Opportunities and limitations of real-time payment systems

What all of these payment solutions have in common is a dedicated clearing system to which several financial institutions are connected. These systems can only work if all participants – the ordering bank and the beneficiary bank – are connected to the system. This is one aspect where providers are partially still working on solutions.

At the moment, each of these clearing networks is confined to its own infrastructure. It ends where the system ends, and is therefore limited. Consequently, none of these systems is really suited to the payments needs of global businesses who frequently make cross-border transfers. This is why the global SWIFT Network has launched SWIFT for Corporates – an initiative that forms part of the global payments innovation project SWIFT gpi and specifically caters to businesses.

What solutions do globally active businesses need?

Instant payments for the SEPA area, Faster Payments for the UK and Real-Time Payments in the US – all of these clearing systems offer payments processing within seconds but, as mentioned, are confined to the limits of their own networks. What globally active businesses really need is a fast and transparent solution for cross-border payments.

SWIFT gpi: fast payments without borders

SWIFT has established a cross-border network that incorporates around 10,000 banks worldwide. In January 2017, it launched the gpi Service that can be used to process global payments in a fast and traceable manner. The objective is for every one of the SWIFT Network banks to offer 24-hour payment processing by the end of 2020. Around half of all gpi payments are credited to the beneficiary within 5 minutes, 95 percent within a day.

How SWIFT gpi works

What’s so special about this new technology is the continuous end-to-end tracking by way of a gpi reference: the Unique End-to-End Transaction Reference (UETR). You can compare the UETR to the tracking number of a parcel: The UETR represents a unique and unalterable reference for every gpi payment. Thanks to this reference, every payment order is not only fully digitized and therefore extremely fast, but you also have a means of tracing the bank where a payment is currently located. SWIFT gpi enables speed and transparency for both cross-border payment status and fees.

The SWIFT for Corporates project

In November 2018, SWIFT launched the SWIFT gpi for Corporates project in order to enable corporates to directly benefit from the gpi technology. The objective was to offer corporates a solution for initiating gpi payment orders directly in their payments system.

Coupa Treasury offers integrated SWIFT gpi technology. The system generates the unique and unalterable tracking reference UETR that is required for gpi payments. In addition, Coupa Treasury automatically processes incoming gpi status messages, enabling users to check the status of a payment at any time.

Corporates need a SWIFT BIC (Business Identifier Code) to make use of SWIFT gpi for Corporates technology. They register their BIC for gpi for Corporates and connect financial institutions that offer gpi for Corporates. All in all, SWIFT gpi for Corporates unlocks completely new opportunities for automating treasury processes, in turn leading to efficiency gains and increased security.

Payments in real-time: our conclusion

While clearing systems such as Instant Payments, Faster Payments or Real-Time Payments present new opportunities for consumers and E-commerce, they are non-integrated solutions and don’t enable payments across different systems. Conversely, the EBICS SEPA Instant Credit Transfer standardization efforts and the SWIFT gpi for Corporates project do offer real potential for corporate treasury: they make payments fast, traceable and transparent: a real leap for corporate payments.

Time to discover Coupa's range of treasury services.