Drive smarter spend strategies with AI

See what exceptional performance looks like and learn how to close the gaps.

Get the Benchmark Report

Drive smarter spend strategies with AI

The Total Spend Management Annual Benchmark Report

Using liquidity most efficiently is in every company’s best interest. Ways to pool liquidity that help companies optimize liquidity planning and management include netting and cash pooling. Companies with existing cash pools can go a step further and completely eliminate intercompany cash flows by implementing netting. Settlement on intercompany accounts at the end of a netting run replaces physical bank account transfers. This process establishes a de-facto in-house bank with all the associated benefits leveraging netting and cash pooling.

Further reading: Netting: An Immersive Guide to Global Reconciliation

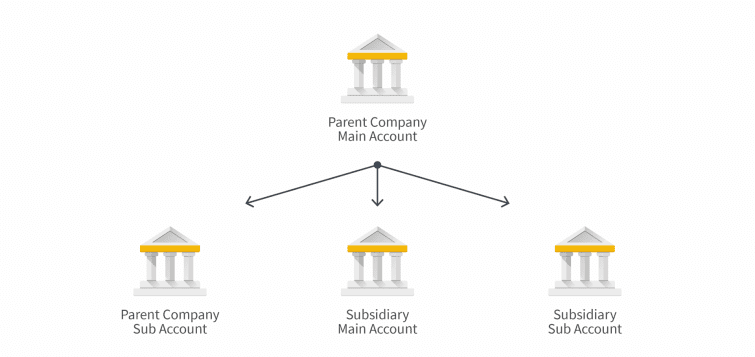

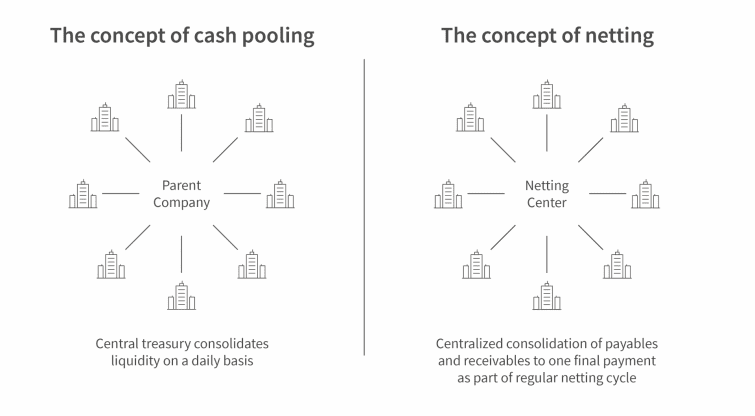

Cash pooling refers to the consolidation of liquidity within one group: Companies can deduct funds from entities with surplus liquidity and provide intercompany loans to entities who are short of funds. Central treasury is usually the one to offset balances.

Technically, this is realized by setting up a master account, which companies use to manage their subsidiaries’ investments and borrowing. Zero balancing, the most common type of cash pooling, operates with sweeps that leave all subsidiary accounts with a balance of zero. End-of-day sweeps automatically pool and consolidate the balances of all accounts on one single account.

Companies have the option of setting up cross-currency cash pools. The more common approach is cash pools in one currency, i.e. one cash pool for USD, one for EUR etc. Cash pooling centralizes FX management, which enables efficient, group-wide hedging.

Companies who use netting offset payables and receivables between two parties and consolidate them in one final payment. Netting with more than two parties involves a central netting center that reconciles payables and receivables and consolidates them. The netting center is usually part of the central treasury.

A netting process can be divided into four steps:

1) Data import

Payables and receivables are imported from ERP systems to the netting system. Alternatively, entities submit their data to the netting center.

2) Data reconciliation

The netting system automatically reconciles the payables and receivables that have been submitted. The result is represented in a netting statement.

3) Information from netting center

Netting participants receive the netting statement detailing the end sum in the requested currency.

4) Close of cycle

The netting center distributes payments to subsidiaries with positive balances. Subsidiaries with negative balances make one netted payment to the netting center.

Companies normally use netting to settle intercompany trade. However, netting can also involve non-group participants.

For currency netting, companies can use pre-defined internal exchange rates. These rates are determined before the start of a netting cycle and apply to all participants. Just as for cash pooling, this centralizes FX management and transfers it to the central treasury.

Taking a look at the elements that cash pooling and netting have in common, you quickly realize: Both make use of a central intermediary to balance liquidity internally, i.e. consolidate and pool it.

Netting in itself reduces the number of payment transactions to one final transaction for each participant, while cash pooling eliminates even this final transaction. Instead of actually making a payment to the cash pool at the end of the netting run, the sum is only booked on the participant’s account. You do not need to make any physical payment. This way, central treasury becomes the netting participants’ financial intermediary. Effectively, you have established an in-house bank.

An in-house bank, set up by way of cash pooling and netting, provides a number of advantages to businesses:

An in-house bank has the potential to transform a business – especially in combination with a treasury management system like Coupa Treasury that promotes collaboration.

Coupa Treasury integrates all entities in all processes, while central treasury maintains overall control. On one hand, this collaboration relieves entities of the burden of complex liquidity planning, payments and FX hedging processes. On the other hand, this kind of collaboration in one system maximizes transparency and visibility of group-wide liquidity and exposure in real time.

Coupa Treasury enables subsidiaries and the central treasury to take care of all tasks together, from cash positioning to processing payments or financing and hedging.

This is an overview of what they achieve together:

Companies who implement netting or cash pooling significantly boost the efficiency of their cash and FX management. Companies who implement both, effectively create an in-house bank.

The collaborative approach of Coupa Treasury helps you set up an in-house bank with very little administrative effort and brings transparency, visibility, efficiency and security to both subsidiaries and the central treasury.

Oh! It looks like you opted out from using the needed cookies. If you are interested in using the AI Agent, then please opt-in to the cookies in the preference center.

Update preferences